VAT Implications UK Explained: Rules, Threshold & Compliance

Understanding VAT implications is essential for any business operating in the United Kingdom. Businesses that sell goods or services must follow UK VAT rules for businesses set by HM Revenue & Customs (HMRC) under the UK Government tax system.

Many business owners still ask common questions. They want to know how VAT works in the UK. Others ask whether VAT applies to profit or turnover. Some businesses also want to understand VAT registration rules in the UK and the penalties for non-compliance.

This guide explains the key UK VAT implications for businesses, including VAT registration thresholds, VAT responsibilities, Brexit changes, and HMRC compliance rules. The goal is simple. Help businesses understand VAT and manage their tax responsibilities correctly.

What are the VAT implications for businesses in the UK?

UK VAT implications refer to the tax responsibilities businesses must follow when dealing with Value Added Tax in the UK. These responsibilities include VAT registration, charging VAT on taxable sales, submitting VAT returns to HMRC, and maintaining proper VAT accounting records. Businesses must monitor their taxable turnover, follow official VAT rules, and comply with HMRC reporting requirements.

| VAT Element | Explanation |

| Output VAT | VAT charged on sales to customers |

| Input VAT | VAT paid on business purchases |

| VAT Returns | Reports submitted to HMRC |

| VAT Invoices | Proof of VAT charged on transactions |

| VAT Compliance | Following official UK VAT regulations |

If businesses fail to follow these requirements, HMRC may impose penalties or interest charges.

How VAT Works in the UK Tax System

To understand UK VAT implications, businesses must first understand how the VAT system works.VAT is a consumption tax added at each stage of the supply chain. Businesses charge VAT on the value they add to goods or services.

When a business sells a product, it collects output VAT from customers. When it buys goods or services, it pays input VAT to suppliers. Businesses can usually reclaim input VAT on qualifying business expenses.

Example of VAT Accounting

| Transaction | Amount | VAT |

| Product Sale | £100 | £20 VAT |

| Business Purchase | £50 | £10 VAT |

| VAT Payable | £20 − £10 | £10 owed |

This example shows how VAT accounting works for UK businesses. Most goods and services fall under the standard VAT rate of 20%.

Standard VAT Rates in the UK

| VAT Rate | Example |

| 20% Standard Rate | Electronics, professional services |

| 5% Reduced Rate | Home energy and certain renovations |

| 0% Zero Rate | Children’s clothing and basic food items |

These rules are governed by the VAT Act 1994, which forms the legal framework for VAT compliance in the UK.

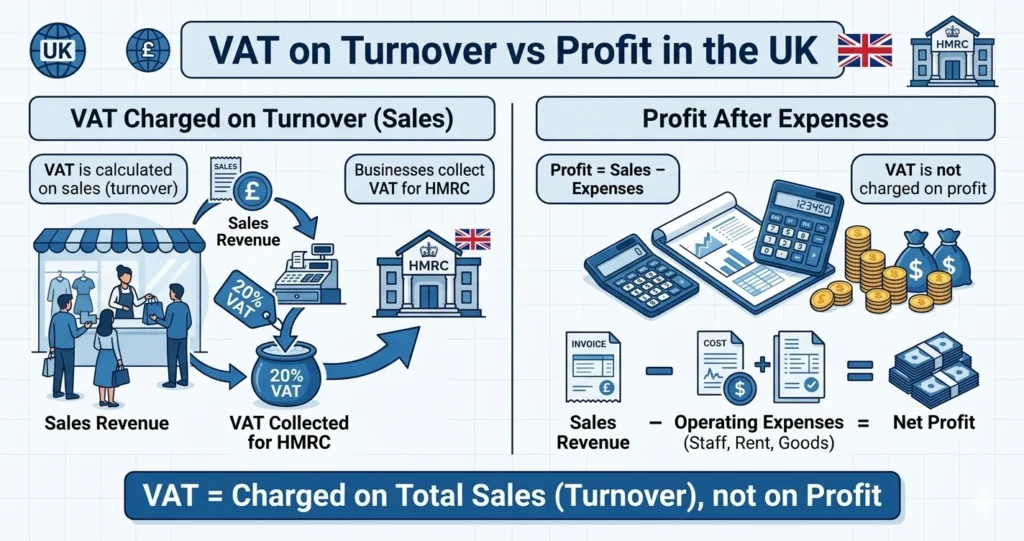

VAT on Turnover vs Profit Explained

A common misunderstanding about UK VAT implications involves whether VAT applies to profit or turnover. The correct answer is simple. VAT is based on taxable turnover, not profit.

Turnover vs Profit Example

| Category | Amount |

| Total Sales (Turnover) | £100,000 |

| VAT Collected (20%) | £20,000 |

| Expenses | £60,000 |

| Profit | £40,000 |

In this example, VAT applies to the £100,000 turnover, not the £40,000 profit. Businesses must charge VAT on sales once they become VAT registered, regardless of whether the business is profitable. Understanding this rule helps businesses avoid mistakes when filing VAT returns with HMRC.

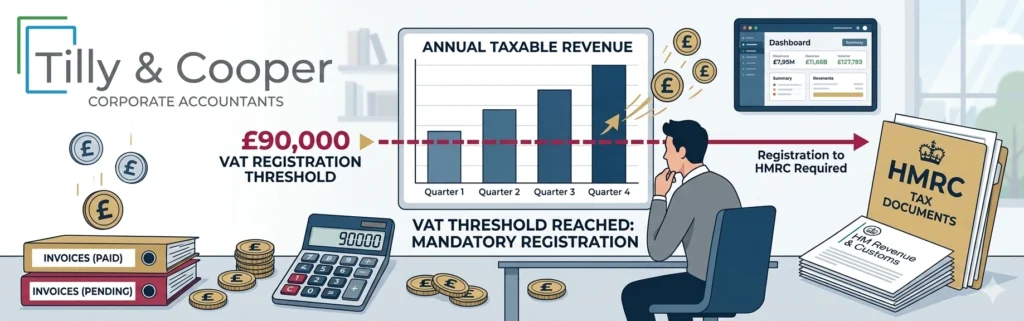

VAT Registration Threshold and Rules in the UK

One of the most important UK VAT implications is knowing when to register for VAT. Businesses must register for VAT when their taxable turnover exceeds the official threshold.

Current VAT Threshold

| Requirement | Amount |

| VAT Registration Threshold | £90,000 taxable turnover |

| Voluntary VAT Registration | Allowed below threshold |

Once the threshold is exceeded, businesses must register within 30 days.

Steps for VAT Registration

- Track annual taxable turnover

- Check the VAT threshold regularly

- Register through the HMRC VAT portal

- Receive a VAT registration number

- Start charging VAT on taxable sales

After registration, businesses must submit VAT returns, issue VAT invoices, and maintain accurate accounting records.

Managing VAT records becomes easier when you follow proper Sole Trader Bookkeeping practices that track income and expenses accurately.

Making Tax Digital (MTD) for VAT

The UK government introduced Making Tax Digital (MTD) to modernize the tax system. Under MTD rules, most VAT-registered businesses must keep digital records and submit VAT returns using compatible accounting software. Businesses must use approved software that connects directly with HMRC systems.MTD helps improve tax accuracy and reduces errors in VAT reporting.

Many businesses now use accounting tools such as:

- QuickBooks

- Xero

- Sage Accounting

Digital record-keeping has become a key part of modern VAT compliance for UK businesses.

VAT Implications of Brexit for UK Businesses

Brexit introduced several changes to UK VAT implications, especially for international trade. Before Brexit, businesses traded with EU countries under intra-EU VAT rules. Now imports and exports follow different VAT procedures.

VAT Rules After Brexit

| Transaction | VAT Treatment |

| Import goods from EU | Import VAT applies |

| Export goods to EU | Usually zero-rated |

| Domestic UK sales | Standard VAT applies |

Many businesses now use postponed VAT accounting, which allows import VAT to be declared through VAT returns instead of paying it immediately. Companies that trade internationally must understand these rules to remain compliant with UK VAT regulations.

IR35 and VAT Implications for Contractors

Contractors and freelancers may face additional UK VAT implications, especially under IR35 legislation.IR35 determines whether a contractor operates as an independent business or as a disguised employee.

VAT Implications for Contractors

| Scenario | VAT Treatment |

| Outside IR35 | Contractor charges VAT on services |

| Inside IR35 | Income treated like employment income |

Even when working inside IR35, contractors may still need to charge VAT if their business remains VAT registered. Contractors must also issue proper VAT invoices and submit regular VAT returns.

Benefits and Responsibilities of VAT Registration

VAT registration provides several advantages for businesses.

Benefits of VAT Registration

| Benefit | Description |

| Reclaim VAT | Businesses can recover VAT paid on expenses |

| Professional credibility | Many clients prefer VAT-registered suppliers |

| Growth readiness | Supports larger contracts and expansion |

However, VAT registration also brings additional responsibilities.

VAT Responsibilities After Registration

Businesses must:

- Submit VAT returns on time

- Issue valid VAT invoices

- Maintain accurate financial records

- Follow approved VAT accounting schemes

Many small businesses use simplified schemes such as the Flat Rate VAT Scheme to manage VAT accounting more easily.

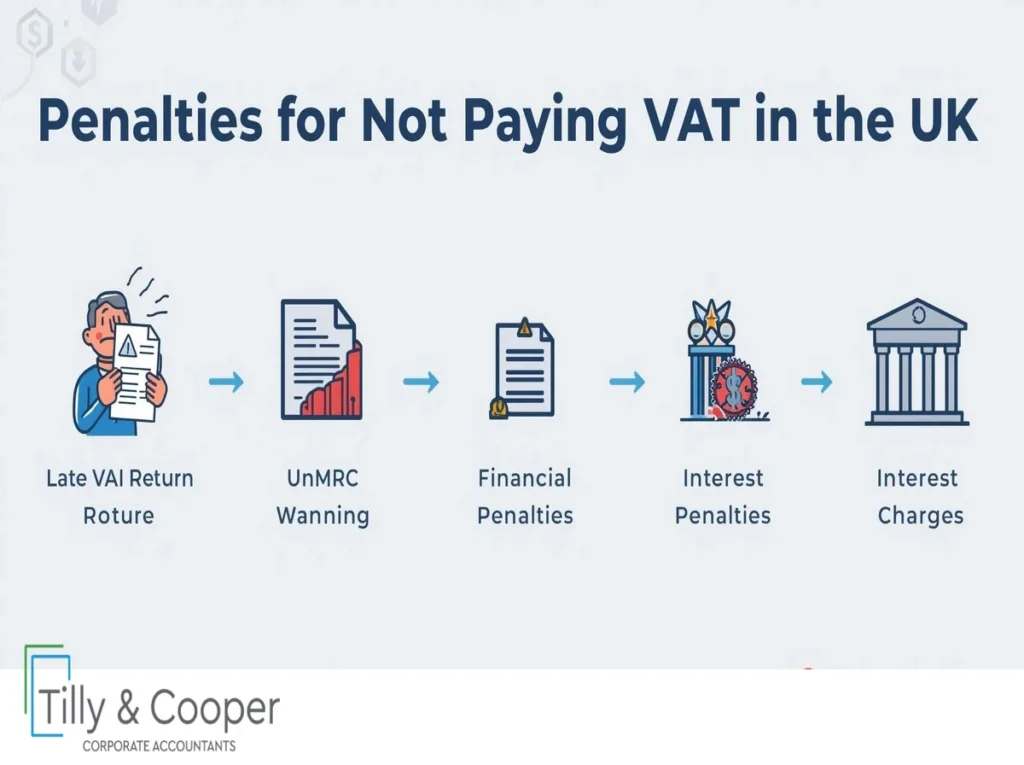

Penalties for Not Paying VAT

Ignoring UK VAT implications can lead to serious consequences.HMRC monitors VAT compliance closely and may investigate businesses that fail to meet their obligations.

Consequences of VAT Non-Compliance

| Violation | Possible Consequence |

| Late VAT Return | Financial penalty |

| Underpaid VAT | Interest charges |

| VAT Fraud | Criminal prosecution |

Common VAT mistakes include:

- Incorrect VAT calculations

- Missing VAT invoices

- Late VAT returns

- Incorrect VAT accounting schemes

Businesses that maintain proper records and follow HMRC guidance can avoid these penalties.

VAT Accounting Schemes in the UK

The UK VAT system offers different VAT accounting schemes that help businesses manage their tax reporting more efficiently. Choosing the correct scheme can simplify accounting and improve cash flow management.

Common VAT Accounting Schemes

| Scheme | Description |

| Standard VAT Accounting | Businesses record VAT when invoices are issued and received. |

| Cash Accounting Scheme | VAT is recorded only when payments are received or paid. |

| Flat Rate Scheme | Businesses pay a fixed percentage of turnover instead of calculating VAT on each transaction. |

| Annual Accounting Scheme | Businesses submit one VAT return per year with advance payments. |

Small businesses often choose simplified schemes to reduce administrative work. Understanding these options helps businesses manage VAT compliance and financial planning more effectively.

Expert Tip

VAT regulations can change when government tax policies are updated. Businesses should regularly check official HMRC guidance or consult a qualified accountant to stay compliant with UK tax law.

Need Help Managing VAT Compliance?

Managing VAT rules, registration requirements, and HMRC reporting can be complex for many businesses.Professional accountants can help ensure accurate VAT records, timely VAT returns, and full compliance with UK tax regulations.

If your business needs help understanding UK VAT implications, expert advice can simplify the process and reduce financial risk.

FAQs

Do businesses pay VAT on profit or turnover?

Businesses pay VAT based on taxable turnover, not profit. VAT applies to the value of sales made by the business.

What is the VAT registration threshold in the UK?

The current VAT registration threshold is £90,000 in taxable turnover within 12 months.

Can businesses reclaim VAT on expenses?

Yes. VAT-registered businesses can reclaim input VAT on qualifying business expenses.

What happens if a business fails to pay VAT?

HMRC may charge penalties, interest, or take legal action depending on the severity of the violation.